Real Estate Agent Bookkeeping Guide

Real estate agent bookkeeping can feel technical because parts of it are. Most agents were never trained in it, and most guides are written for accountants, not commission-based businesses.

But as an independent contractor, you are the one responsible for tracking income, expenses, and profit.

No employer payroll department is doing it for you.

This guide translates bookkeeping into plain language and real-world agent workflows so you can keep clean books without becoming an accountant.

It gives you the knowledge you need to keep clean books without drowning in tax theory or CPA jargon.

Even if you hire a CPA or bookkeeper, responsibility doesn’t disappear, it shifts. Delegation works best when your records, accounts, and processes are organized from the start. The agent who understands their bookkeeping at a working level gets better reports, better advice, and better decisions.

What Real Estate Agent Bookkeeping Is

At its core, bookkeeping is a system for recording and organizing your money activity so your financial data is accurate and usable.

For most real estate agents, bookkeeping is associated mainly with taxes. That’s understandable.

Compared to the chase and hunt of a deal, bookkeeping rarely feels exciting, and much of the conversation around it happens at tax time.

But bookkeeping serves two different purposes:

- Financial reporting: producing clean records for taxes and compliance

- Management insight: helping you understand where your money is going and whether your business is actually profitable

Go Deeper: Management vs financial accounting in real estate

When bookkeeping is treated only as a tax requirement, it becomes a once-a-year chore. When it’s treated as a management system, it becomes a tool for running the business with clarity.

It helps answer the question that plagues many agents: “How did I have such a high GCI — and still not make much money? Where did it all go?”

Good real estate agent bookkeeping helps you:

- Know your true profit; not just production

- Compare marketing spending versus closings

- Spot expense creep early

- Evaluate brokerage splits realistically

- Avoid “high production, low profit” traps

Cash vs Accrual Accounting for Real Estate Agents

Most real estate agents should use cash basis bookkeeping. It’s simpler, more practical, and better aligned with how commission income actually works.

Under cash basis bookkeeping:

- Income is recorded when you receive the money

- Expenses are recorded when you pay them

Example: You close on a property on February 20. Your commission hits your bank account on February 22. Under cash basis, the income is recorded on February 22, the day the money is received.

Accrual accounting works differently.

Income and expenses are recorded when they are earned or incurred, even if no money has changed hands yet. That means transactions may be recorded based on when the work was performed or when a bill is issued, not when payment happens.

For most commission-based agents, that added timing precision doesn’t produce better decisions — it just adds bookkeeping complexity.

Cash basis bookkeeping works well for real estate agents because:

- There is usually no true receivables cycle

- Few unpaid invoices exist

- Commission income is event-based

- Workflows are simpler

- Reports are easier to understand

- It matches how most agents think about money

- It usually matches the tax reporting method used by solo agents

When Accrual May Make Sense

Accrual accounting is more useful when the business structure becomes more complex, such as:

- Operating a brokerage

- Running a large team with layered payroll

- Managing properties

- Operating multiple entities

- Carrying significant payables or receivables

For most solo agents and small teams, accrual accounting adds complexity without meaningful benefit.

Cash basis keeps bookkeeping clear, faster, and decision-usable, which is exactly what most agents need.

Setting Up Your Books

Before we get into tools and workflows, we need to cover the underlying structure that all bookkeeping systems use.

Whether you keep books in software or a spreadsheet, every transaction must be sorted the same basic way. This structure is called your chart of accounts. Think of it as the sorting system behind your bookkeeping — once you understand it, everything else becomes easier.

Real Estate Agent Chart of Accounts

The chart of accounts is one of the most misunderstood — and underused — parts of agent bookkeeping.

Many agents simply accept the default categories their software creates and never adjust them. The result is technically correct bookkeeping, but low-value reporting.

If your buckets aren’t designed around how a real estate business actually operates, your numbers won’t answer the questions you actually have.

A chart of accounts built only for tax filing may group expenses in ways that are technically correct, but not very helpful for running a real estate business.

Agent bookkeeping benefits from categories that also support management decisions, like tracking lead sources, marketing channels, and deal-related costs separately.

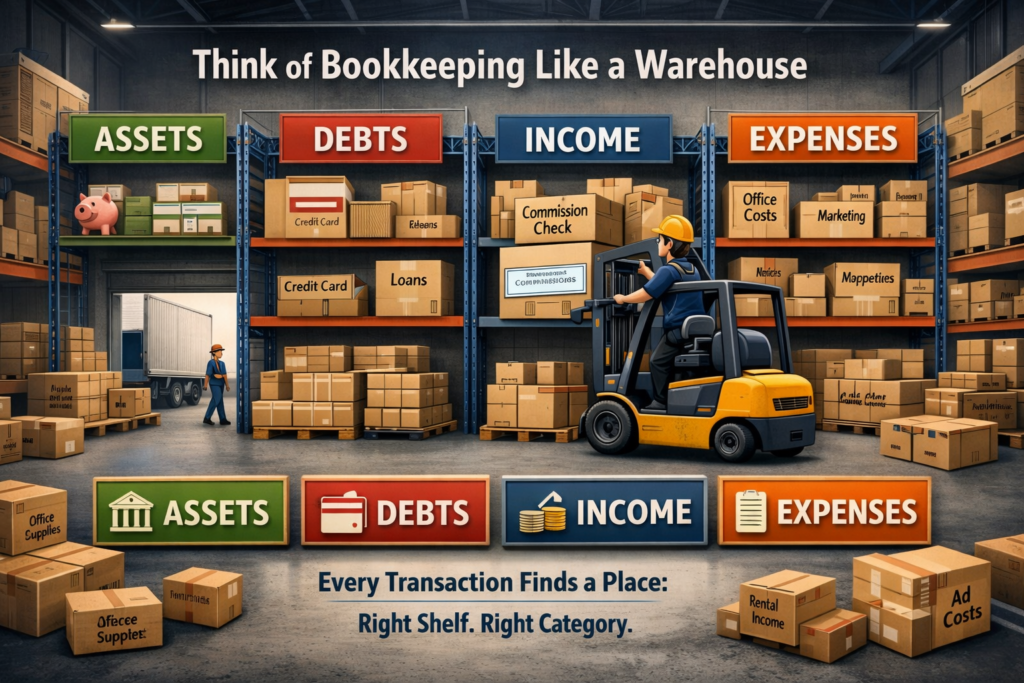

Bookkeeping Like A Warehouse

Your chart of accounts is your bookkeeping sorting system.

It’s how every transaction gets placed into the correct “bucket” so your reports are accurate and useful.

Think of your bookkeeping like a warehouse.

Every dollar that moves in your business is a package that arrives at the loading dock. It must be placed on the correct shelf or your inventory counts (reports) become unreliable.

Each transaction needs a bucket.

Bookkeeping gives you four main warehouse sections:

- Assets: what you own, like bank accounts or cash

- Debts (Liabilities): what you owe, like a credit card

- Income: money coming in, like commission income

- Expenses: money going out, like office expenses or lead generation

Every transaction goes into one of those four levels first, then into a more specific bucket (account) inside that level.

When categorizing a transaction, ask two questions:

- Level question: Which of the four sections does this belong to (asset, liability, expense or income)?

- Bucket question: Which specific account inside that section fits best?

That’s the entire chart of accounts system. For most real estate agents, you will work primarily in two sections day-to-day:

- Income

- Expenses

Assets and debts are usually handled automatically through your bank and credit card accounts once connected to your bookkeeping software.

Practical Chart of Accounts Example (Table)

| Account Type | Account Name |

| Income | Commission Income |

| Expense | Brokerage Fees |

| Expense | Desk Fees |

| Expense | Lead Generation |

| Asset | Bank Account #### |

| Liability / Debt | Credit Card #### |

| Equity | Members Equity |

Every transaction needs a bucket. Pick the level first. Pick the bucket second.

Stay consistent. Consistency matters more than perfection because consistent buckets produce usable reports.

Bookkeeping Options For Real Estate Agents

There is no single “best” bookkeeping tool for every real estate agent. The best system is the one you will actually use consistently and that fits your current stage of business.

All bookkeeping tools — from spreadsheets to full accounting software — follow the same core structure. The difference is how much automation, reporting, and complexity they support.

Start with a system you can maintain. Let business growth push you to upgrade.

Simple Options (Best for Solo and DIY Agents)

For many solo agents and early-stage businesses, simple tools are completely sufficient:

- Spreadsheets

- Real-estate-focused bookkeeping apps like Realtyzam

These options work well when:

- You have no employees

- Few monthly transactions

- Simple commission income

- Minimal reporting needs

- You are doing your own bookkeeping

These solutions are easier to learn and faster to maintain. The tradeoff is less advanced reporting and automation.

That’s usually acceptable early on.

Full Accounting Software (Best as Complexity Increases)

More robust platforms like:

- QuickBooks

- Xero

become more valuable when your business adds complexity, such as:

- Hiring a virtual assistant or employee

- Running payroll

- Managing contractors or team-deals

- Operating a team structure

- Needing deeper reporting

- Delegating bookkeeping to a VA or bookkeeper

These systems are more powerful, but come with a learning curve. Many agents adopt them later and delegate the day-to-day bookkeeping once the business justifies it.

A Practical Rule of Thumb

Start simple. Stay consistent. Upgrade when complexity forces you to. Not before.

Most bookkeeping failures come from choosing a system that is too complex to maintain, not too simple to scale.

The right tool is the one that gets used every week.

Get the real estate agent bookkeeping spreadsheet and start tracking your income and expenses.

Don’t Let Driving Dictate Your Bookkeeping Software Choice

Driving is one of the largest business activities for most real estate agents, which means vehicle tracking and receipt capture matter. But don’t let mileage tracking alone determine your entire bookkeeping solution.

At a high level, there are two ways vehicle expenses are typically tracked for business use:

Mileage method: you track business miles driven and apply the standard mileage rate

Actual expense method: you track actual vehicle costs (fuel, maintenance, insurance, etc.) and allocate the business-use portion

You don’t need to master the tax rules here, but you should know which method you’re using and track consistently. Your tax professional can advise which method is better for your situation.

What matters for bookkeeping is this:

- You must track business driving somehow

- Your tracking method must be consistent

- Your records must be supportable

Many bookkeeping platforms include built-in mileage tracking, but you can also use a separate mileage app and keep your main bookkeeping in a different system. Tools can be stacked. Your bookkeeping software does not have to do everything.

Choose your primary bookkeeping solution based on your overall business needs, then add mileage tracking alongside it if needed.

Make Agent Bookkeeping Less Painful

Use Automation Rules

Bookkeeping feels painful when every transaction has to be categorized manually. The fix is not more discipline. It’s more automation.

Depending on the software or bookkeeping solution chosen, this may be limited.

Most modern bookkeeping tools can learn patterns and apply rules so recurring transactions are categorized automatically. Once set up, these rules quietly handle the repetitive work for you.

Common rule candidates for real estate agents include:

- MLS dues

- Association and board fees

- Brokerage charges

- Software subscriptions

- Marketing platforms

- Recurring vendors

When a transaction always comes from the same vendor and usually belongs in the same category, it should become a rule.

Set it once → categorize it automatically going forward.

A small amount of setup eliminates hundreds of repetitive clicks over a year. That’s one of the biggest leverage points in agent bookkeeping.

Automation doesn’t remove oversight, but it dramatically reduces friction. And lower friction is what turns bookkeeping from avoided to sustainable.

Hire a Real Estate Agent Bookkeeper

At some point, the best bookkeeping optimization is not better software, it’s help.

Hiring a bookkeeper can remove most of the day-to-day recording and reconciliation work, but timing matters. Too early, and you create unnecessary costs. Too late, and your books fall behind and require cleanup.

For many real estate agents, hiring help makes sense when:

- Transaction volume increases

- Monthly categorizing feels consistently behind

- You’ve fallen several months out of date

- Your time is better spent on revenue work

- Your business structure is getting more complex

A bookkeeper’s role is to maintain accuracy and consistency. Not to run your business decisions. They record, reconcile, and organize. You still review and interpret.

A practical model that works well for many agents:

- You provide structure and contex

- They provide consistency and accuracy

Even with a bookkeeper, you should still:

- Review monthly reports

- Answer category questions

- Confirm unusual transactions

- Look at your profit and loss regularly

Delegation reduces workload. Oversight preserves usefulness.

When done right, hiring a bookkeeper turns bookkeeping from a personal burden into a managed system without losing visibility into your numbers.

Giving Everything to the CPA at Year End

Some real estate agents try to avoid bookkeeping during the year by saving everything and sending it to their CPA at tax time.

It sounds efficient, but in practice, it usually isn’t.

Year-end cleanup is not the same as ongoing bookkeeping.

When records are organized monthly, transactions are categorized while still fresh, receipts are available, and questions can be answered quickly.

When everything is deferred to year end, your tax professional is forced into reconstruction work — sorting, guessing, and clarifying months after the fact.

That reconstruction time is rarely cheaper. Often, it costs more.

More importantly, year-end-only bookkeeping produces numbers too late to help you run the business. You lose visibility into:

- Marketing return on investment

- Expense creep

- Net profit trends

- Split and brokerage cost impact

- Cash flow patterns

A CPA’s primary role is tax reporting and compliance. A bookkeeper’s role is ongoing record maintenance. They solve different problems at different times.

Monthly bookkeeping gives you usable financial information all year. Year-end cleanup gives you a tax return and little else.

Consistent records beat last-minute reconstruction every time.

Practical Bookkeeping Tips for Real Estate Agents

These are high-impact bookkeeping practices that don’t require complex accounting knowledge — but can significantly improve the usefulness of your records.

Track Deal Costs Separately

Some expenses are directly tied to specific transactions. When you track them separately from general overhead, your reports become much more useful.

Common deal-level costs include:

- Listing photography

- Property staging

- Transaction coordination per file

- Referral payouts

- Co-op commissions you pay

You can group these under a category such as: Direct Deal Costs or Cost of Sales

Tracking these separately allows you to see:

- Profit per closing

- Profit by listing vs buyer side

- Profit after deal-specific spend

This is especially helpful when evaluating lead sources and marketing strategies.

Inside software programs, like Quickbooks, you can often view this by tying expenses at the project level. Unfortunately, this functionality is one of the higher priced bookkeeping options for real estate agents.

How to Record Commission Income

There are two common ways real estate agents record commission income in their books. Both can be technically acceptable — but they produce very different management insight.

Many agents simply record the net deposit that hits their bank account. It’s easy, but it hides important business information.

A more decision-useful method is to record gross commission income and brokerage splits separately.

Method 1: Net Deposit Only

This method is simple and common,but it blends your brokerage cost into the deposit and removes visibility into how much you are actually paying to your broker.

That makes it harder to evaluate: Brokerage value vs cost, split changes, cap structures, and brokerage ROI

Example:

- Gross commission: $15,000

- Brokerage keeps: $4,500

- You receive: $10,500

Books show: Income = $10,500

Net method is most reasonable when you want maximum simplicity, have low production volume, strictly bookkeeping for taxes, and you do not analyze brokerage economics.

Method 2: Gross Income

Using the same deal, you would record:

- Income = $15,000

- Brokerage Split Expense = $4,500

- Net Profit Impact = $10,500

This method treats your brokerage split as a true business expense, which it is. You may not physically receive the full commission first, but you economically earn it and contractually assign a portion to the brokerage.

This approach gives you better visibility into:

- True production vs retained income

- Brokerage cost percentage

- Split impact on profit

- When switching brokerages would improve margins

For agents who want management insight — not just tax records — this method is usually more informative.

If you want bookkeeping for compliance only, the net method is acceptable. If you want bookkeeping for decision-making, the gross + split method is stronger.

Advanced Real Estate Agent Bookkeeping Tip

Bookkeeping tells you what already happened. Activity metrics help predict what will happen next. When you connect the two, your books stop being historical records and start becoming a planning tool.

Your financial records show results, but your activity creates those results. When you measure both, you can estimate the economic value of your actions and set smarter targets.

Example:

800 outbound calls → $64,000 in commissions

Each call ≈ $80 of commission value

Now your activity targets help forecast revenue. If you want to grow income, you don’t guess — you increase the right activities.

This only works when your bookkeeping is clean enough to trust the revenue numbers and your activity tracking is consistent enough to compare.

Useful activity-linked metrics for real estate agents include:

- Revenue per lead source

- Revenue per listing taken

- Revenue per buyer consult

- Revenue per signed client

- Cost per closing

- Marketing cost per deal

Once you can see both sides — activity and financial outcome — you can adjust behavior earlier instead of waiting for year-end results.

This is where bookkeeping shifts from recordkeeping to operational guidance.

Common Real Estate Agent Bookkeeping Mistakes

Most bookkeeping problems for real estate agents aren’t caused by complex rules, they come from a few repeated habits that quietly reduce accuracy and usefulness. Avoiding these common mistakes will keep your books cleaner and your reports more decision-useful.

Mixing Personal and Business Spending

Using personal accounts or credit cards for business expenses creates confusion, missed deductions, and messy reports. Open and use dedicated business accounts whenever possible. Clean separation makes everything easier — categorizing, reconciling, and reviewing.

Recording Commission Income Incorrectly

Many agents record commission deposits without a consistent method — sometimes net, sometimes gross, sometimes split differently each time. Pick a method (net deposit or gross with split expense) and apply it consistently so your reports stay comparable month to month.

Skipping Monthly Reconciliation

If you don’t reconcile your bank and credit card accounts monthly, errors and missing transactions compound. Reconciliation is what confirms your books match reality. Without it, your reports are guesses.

Not Capturing Receipts and Supporting Documents

Uncaptured receipts lead to uncategorized expenses, weak audit support, and forgotten deal costs. Capture receipts when the transaction happens, not months later. Documentation habits matter more than software features.

Creating Too Many Categories

Over-detailed charts of accounts make bookkeeping harder and slower without improving decisions. More categories do not automatically mean better insight. Use enough buckets to be useful, not so many that categorizing becomes friction.

Waiting Until Tax Season

Backfilling a year of bookkeeping turns a simple maintenance task into a cleanup project. It also removes your ability to use the numbers during the year. Monthly bookkeeping creates control. Annual bookkeeping creates stress.

Treating Bookkeeping Like Accounting

Bookkeeping is about recording and organizing transactions consistently. It does not require tax law expertise or complex accounting judgments. Overcomplicating bookkeeping leads to avoidance. Keep it structured, simple, and repeatable.

The Goal of Real Estate Agent Bookkeeping

The goal of real estate agent bookkeeping is not just to satisfy your CPA or file a tax return once a year. It’s to give you clear, usable financial visibility so you can run your business with confidence.

When your bookkeeping is consistent and well-structured, it becomes more than recordkeeping — it becomes a decision tool.

Good bookkeeping helps you:

- Know your true profit — not just your production numbers

- See which marketing actually produces return on investment

- Manage the ups and downs of commission-based income

- Make smarter operating and growth decisions

- Reduce tax-season stress and cleanup work

- Scale your business with better financial control

You don’t need perfect books. You need current, consistent, decision-useful books.

Start simple. Stay consistent. Improve the structure as your business grows. That’s what turns bookkeeping from a burden into an advantage.